Workers Compensation Insurance Requirements

Requirements for Workers Compensation Insurance

Types of Coverage

New Jersey law requires that all New Jersey employers not covered by federal programs have workers’ compensation coverage or be approved for self-insurance. Even out-of- state employers may need workers’ compensation coverage if a contract of employment is entered into in New Jersey or if work is performed in New Jersey.

Coverage may be obtained in one of two ways:

Workers’ Compensation Insurance Policy written by a mutual or stock carrier authorized to write insurance in New Jersey. Premiums for such insurance are based on the classification(s) of the work being performed by employees, the claims experience of the employer, and the payroll of the employer.

Self-Insurance through application to and approval by the Commissioner of the Department of Banking and Insurance. Approval for self-insurance is based upon the financial ability of the employer to meet its obligations under the law and the permanence of the business. The posting of security for such obligations may be required.

A self-insured employer has the option of administering its own workers’ compensation claims or contracting with a third-party administrator (TPA) to provide these services. For more information about self-insurance, please refer to N.J.S.A. 34:15-77 of the New Jersey Workers’ Compensation statute or contact the Department of Banking and Insurance at (609) 292-5350, ext. 50099.

Note: Governmental agencies are required to provide workers’ compensation benefits to their employees but are not required to purchase insurance or receive approval as a self- insurer. They generally either 1) obtain an insurance policy, 2) participate in an insurance pool, or 3) maintain a separate appropriation for workers’ compensation.

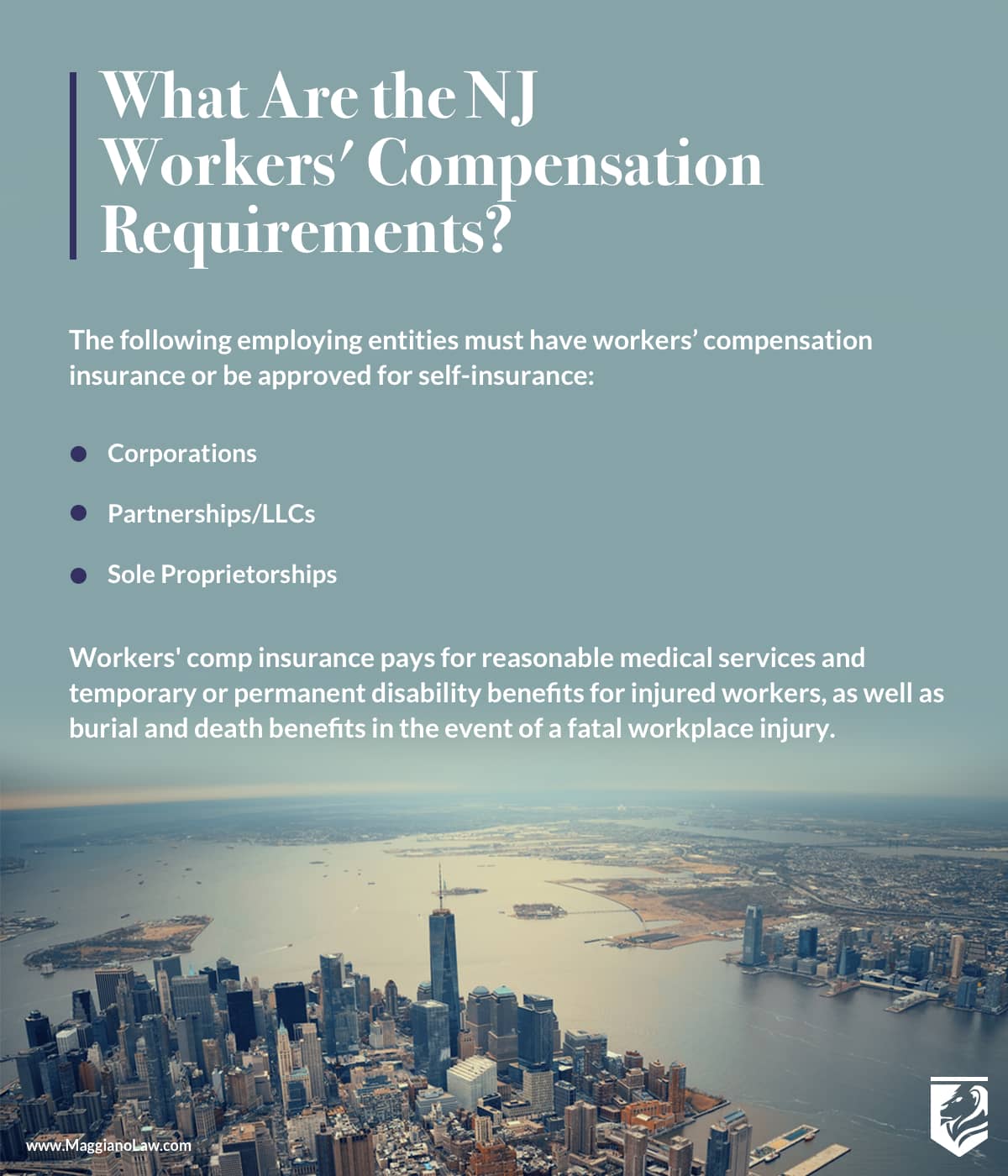

The following employing entities must have workers’ compensation insurance in effect:

- Corporations — All corporations operating in New Jersey must maintain workers’ compensation insurance or be approved for self-insurance so long as any one or more individuals, including corporate officers, perform services for the corporation for prior, current or anticipated financial consideration.*

- Partnerships/LLCs — All partnerships and limited liability companies (LLCs) operating in New Jersey must maintain workers’ compensation insurance or be approved for self-insurance so long as any one or more individuals, excluding partners or members of the LLC, perform services for the partnership or LLC for prior, current or anticipated financial consideration.*

- Sole Proprietorship — All sole proprietorships operating in New Jersey must maintain workers’ compensation insurance or be approved for self-insurance so long as any one or more individuals, excluding the principal owner, performs services for the business for prior, current or anticipated financial consideration.*

*Financial consideration means any remuneration for services and includes cash or other remuneration in lieu of cash such as products, services, shares of or options to buy corporate stock, meals or lodging, etc.

Definition of “Employee”

The New Jersey Workers’ Compensation Act is liberally interpreted with respect to the definition of “employee” and is broader than the Internal Revenue Code and Unemployment Compensation statute. A variety of working relationships have been determined to be that of an employer-employee, including some that would not appear to be a typical employment situation. Further, a contract or other agreement as to whether an individual is an employee is not binding in determining whether an employee— employer situation is present.

New Jersey courts, in deciding this issue, have developed two tests: the “control test” and the “relative nature of the work test.”

Under the “control test,” the relationship between a business and the individual is re- viewed. There is employment if the business retains the right to supervise the individual and control what is done as well as how it shall be done.

Under the “relative nature of the work test,” there is employment if an individual relies on income from the business and the work performed by the individual is an integral part of the activities of the business.

If any or both of these tests are met, an employee—employer relationship is established.

Obtaining Workers’ Compensation Coverage

The New Jersey Compensation Rating and Inspection Bureau (NJCRIB), an agency in the New Jersey Department of Banking and Insurance, is responsible for establishing and maintaining regulations and premium rates for workers’ compensation and employers’ liability insurance.

Workers’ compensation insurance coverage can be obtained from any of the more than 400 private licensed insurance companies authorized to sell workers’ compensation policies in New Jersey. A policy can be purchased directly from an insurance carrier, an insurance agent, or an insurance broker.

For assistance with obtaining coverage, please contact: New Jersey Compensation Rating and Inspection Bureau 60 Park Place Newark, NJ 07102 www.njcrib.com (973) 622-6014

Insurance Premium Rates

The primary device used to determine workers’ compensation insurance premiums is the classification system, which groups New Jersey businesses into various classifications. The purpose of this system is to bring together, within each classification, employers engaged in the same type of business.

Accompanying each classification is a rate that represents the average work-injury experience for that classification. This rate is adjusted annually according to the latest available work-injury experience data.

It is also recognized that no two employers, although they may be in the same business, have exactly the same operations or identical conditions of employment. Within any given classification, there are employers with better-than-average work injury experience and those with worse-than-average work injury experience. To account for such differences, an additional refinement to the classification system is offered through an- other program known as the Experience Rating Plan. In this plan, an employer’s own work injury experience is used to modify its premium, higher or lower, by comparing it to the average work-injury experience of all employers in the classification to which the employer is assigned.

For more information on how rates are established, you may wish to read the WC Reference Guide available on NJCRIB’s Web site www.njcrib.com1ReferenceGuidelcribcnst.asp

What a Workers’ Compensation Policy Covers

A workers’ compensation policy covers the following:

- For injured employees: Reasonable medical services necessary to treat the job injury or illness Temporary disability benefits to help replace lost wages up to statutory maximum Permanent disability benefits to compensate for the continued effects of the injury Burial and death benefits for dependents in cases of fatal injury

- For employers: Coverage of financial liabilities for work-related injuries and illnesses Legal representation

Penalties for Failure to Insure

The consequences for failure to provide workers’ compensation coverage can be very significant, even without a work-related injury. Specifically, the law provides that failing to insure is a disorderly persons offense and, if determined to be knowing, a crime of the fourth degree.

Penalties for such failure can be assessed up to $5,000 for the first 10 days with additional assessments of $5,000 for each 10-day period of failure to insure thereafter. In the case of a corporation, liability for failure to insure can extend to the corporate officers individually. Penalties assessed for failure to insure are not dischargeable in bankruptcy.

Where a work-related injury or death has occurred, the employer, including individual corporate officers, partners or members of an LLC, is directly liable for medical expenses, temporary disability, and permanent disability or dependency benefits. In addition to awards for medical expenses and other benefits, New Jersey law also provides for civil penalties against the employer and its officers where failure to insure is determined. Awards and penalties arising from these claims can become liens against the uninsured employer and its officers, which are generally enforceable in the New Jersey Superior Court against any assets belonging to the uninsured employer and its officers.